Introduction:

With the global adoption of electronic invoicing, there is sometimes confusion about what constitutes an electronic invoice(e-invoice), especially when the adoption is new in a country.

Let’s start with the definitions according to the Collins dictionary:

Invoice – “An invoice is a document that lists goods that have been supplied or services that have been done, and says how much money you owe for them”

Electronic – “involving or concerned with the representation, storage, or transmission of information by electronic systems”.

Based on the above definitions, we can summarize that an invoice is a document that lists items or services provided and the amount due. When it’s electronic, this means it’s created, stored, or sent using electronic systems.

For tax purposes, invoices must meet specific requirements to be accepted as tax invoices, which can vary depending on the jurisdiction. It’s important to note that electronic invoicing is not solely adopted for tax purposes, its implementation can vary based on a country’s needs and the problem its government aims to solve.

For example, in Australia, electronic invoicing is not mandatory yet. The primary aim of introducing e invoicing is to facilitate the way of doing businesses and streamline processes. Presently, the Tax Administration can’t access detailed invoice data, it only has access to high level aggregate data. It is expected that in the future, the adoption of electronic invoicing in Australia will become mandatory.

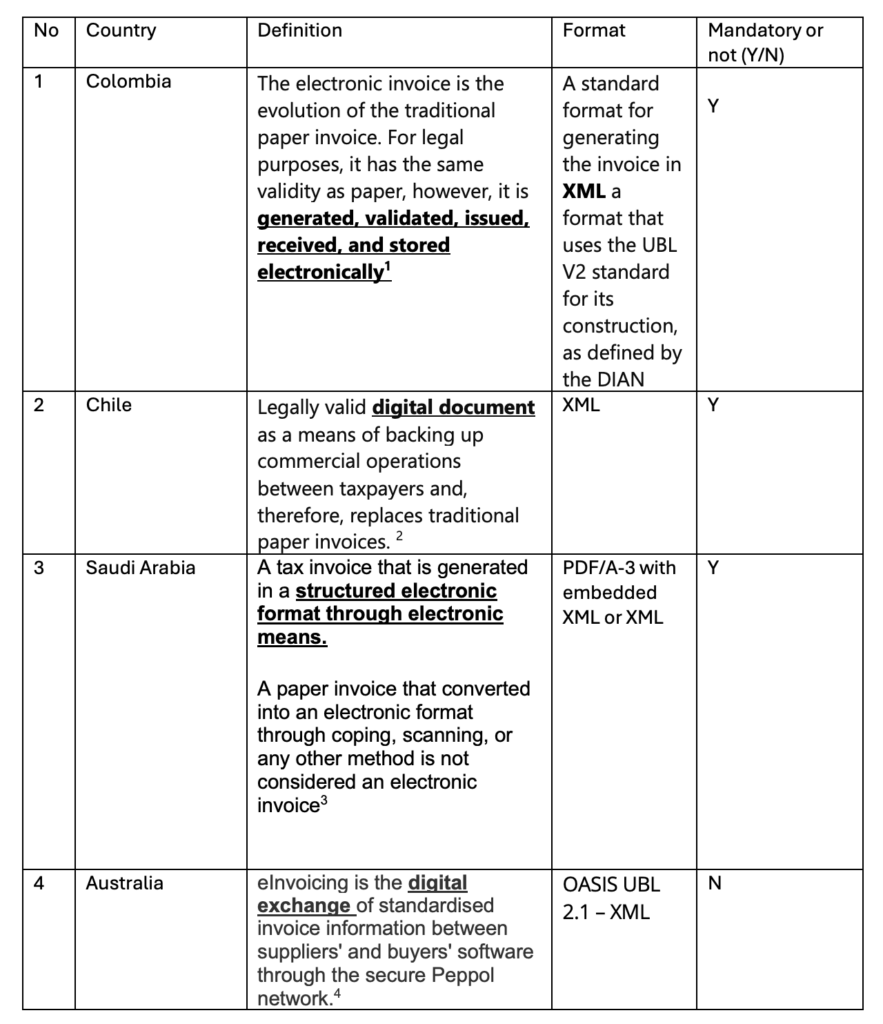

Definitions from Tax Administrations and government entities:

The motivation for implementing electronic invoicing at country level depends on three key aspects:

1) The specific problem that the implementation of e-invoicing aims to solve.

2) Whether the adoption of e-invoicing is mandatory

3) The anticipated developments following the implementation of e-invoicing.

To clarify what defines an e-invoice, e-invoicing and what does not, we have compiled different definitions from various tax administrations, free trade agreements in the table below: